Natural gas

Natural gas trade

We expect U.S. liquefied natural gas (LNG) exports in the third quarter of 2026 (3Q26) to average 16.5 billion cubic feet per day (Bcf/d), down 0.2 Bcf/d compared with last month’s forecast. In July, international prices rose to levels last reached in early April, as LNG vessel traffic through the Strait of Hormuz slowed considerably after strikes on vessels resumed on July 7. Maintenance at Freeport LNG began on July 10 and is expected to be completed in late August, affecting 2.0 Bcf/d of nominal export capacity in the short-term. However, even with Freeport fully operational, exports would remain limited due to slow growth in additional export capacity despite U.S. price spreads to Europe and Asia remaining elevated due to ongoing disruptions.

Maintenance at Freeport and other LNG export terminals have reduced feedgas demand on the Gulf Coast in June and July. Reduced demand has helped boost storage inventories in the South Central region to 5% above the five-year average (2021–2025) as of the week ending July 31, compared with inventories that were almost equal to the five-year average during the week ending May 29, according to our Weekly Natural Gas Storage Report.

We estimate total U.S. natural gas exports by pipeline will average 9.6 Bcf/d in 2026 and rise to 10.0 Bcf/d in 2027, up from 9.5 Bcf/d in 2025. This growth is due to rising demand from the new Energia Costa Azul LNG terminal, which is supplied by the U.S. Permian Basin and shipped its first cargo on July 8, bringing 0.4 Bcf/d of nominal export capacity online in Mexico’s Pacific Coast. In addition, U.S. natural gas exports to Mexico have increased to supply natural gas-fired power plants that have been brought online this year, driven by stronger demand in Mexico as Energia Costa Azul and natural gas-fired power plants ramp to full capacity.

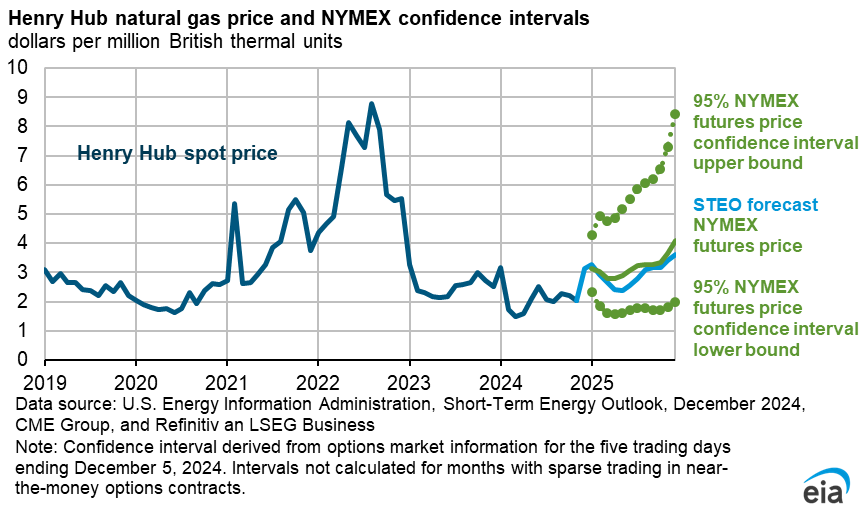

Natural gas prices and storage

We expect the Henry Hub spot price to average $2.87 per million British thermal units (MMBtu), in 3Q26, down 50 cents compared with last month's forecast. Our lower price forecast reflects reduced LNG feedgas demand and record natural gas production, which we expect will leave natural gas inventories at their highest level heading into winter since 2016. We expect Henry Hub prices to rise gradually in the coming months but remain relatively low because inventories are well above the five-year average. Futures prices show a similar pattern, with contracts through September 2026 remaining below $3.00/MMBtu.

In this forecast, we expect natural gas inventories to be a record 3,985 billion cubic feet (Bcf) at the end of October 2026, which is an increase of 19 Bcf compared with the July STEO and 5% above the five-year average. With high storage heading into winter, we expect the Henry Hub spot price will remain below $3.00/MMBtu until November and average $3.03/MMBtu over the remaining five months of the year, nearly 50 cents/MMBtu lower than last month’s forecast.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}