Release Date: July 11, 2023

STEO Between the Lines: U.S. LNG exports will increase next year as two export terminals come online

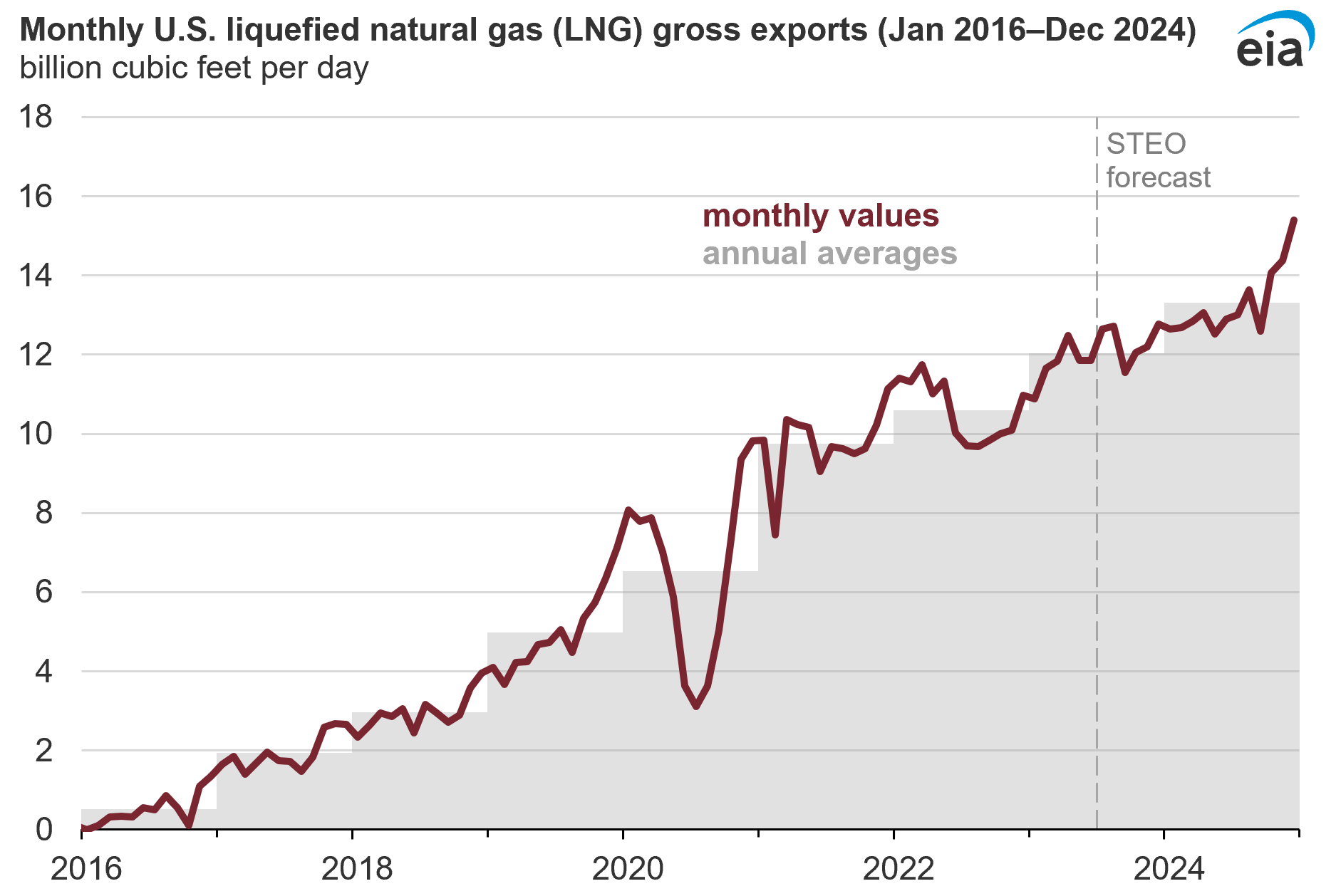

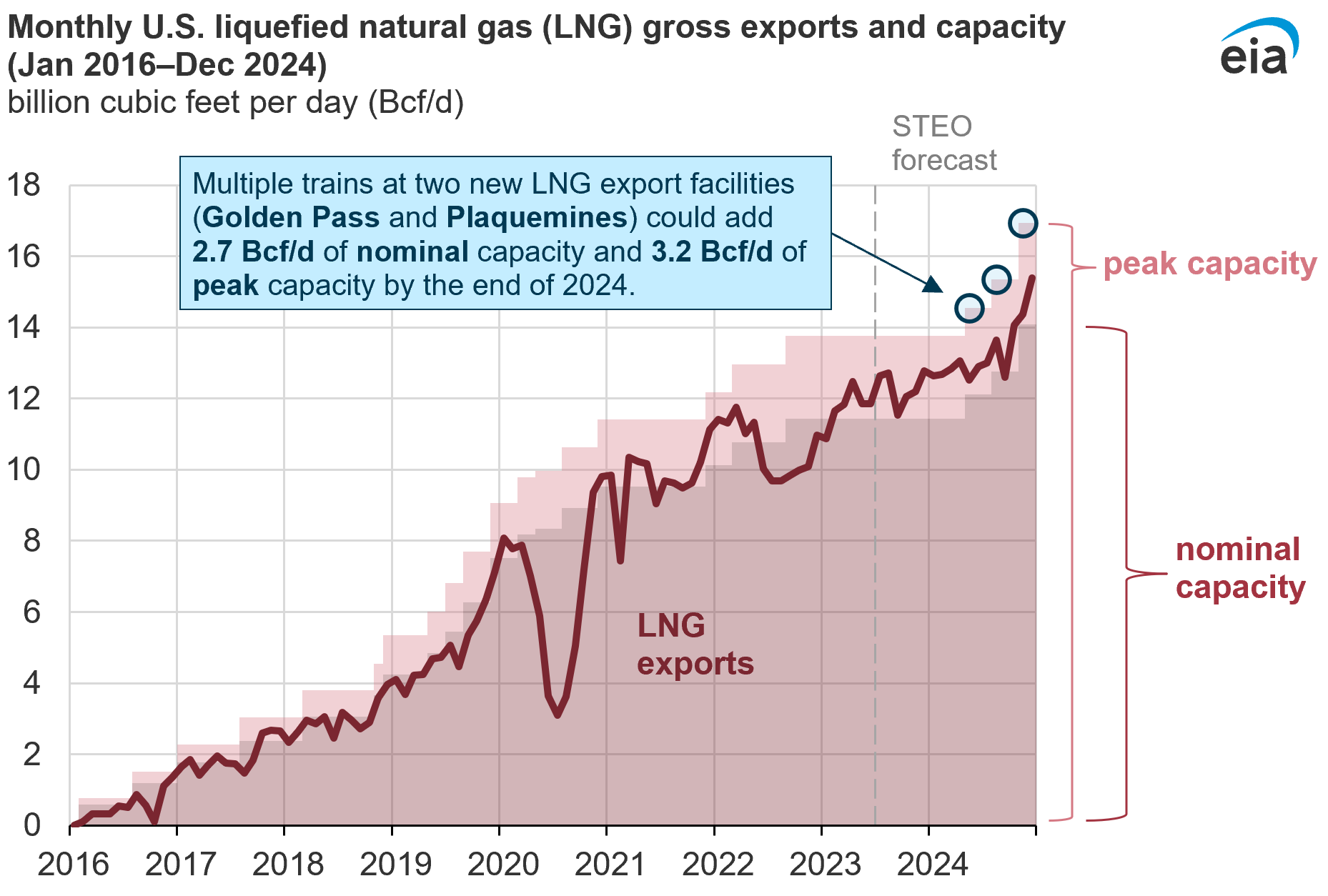

Increases in liquefied natural gas (LNG) exports have helped the United States become a net exporter of natural gas in 2017 and of total energy in 2019. New export terminals increased U.S. LNG exports every year since 2016, positioning the United States among Qatar and Australia as one of the top three LNG-exporting countries in the world. We forecast that U.S. LNG exports will continue to grow in 2024, as two new LNG liquefaction projects come online: Golden Pass in Texas and Plaquemines in Louisiana.

Data values: U.S. natural gas supply, consumption, and inventories

International natural gas market conditions are currently favorable for more U.S. LNG exports. Natural gas prices at several price hubs in Europe and Asia are relatively high compared with U.S. natural gas prices. In our Short-Term Energy Outlook, we assume that U.S. LNG exports will continue to replace pipeline natural gas that had previously been exported from Russia to Europe. Relatively little growth in global LNG export capacity in the next two years will increase demand for flexible LNG supplies, mainly from the United States, to meet incremental growth in global demand.

We expect U.S. LNG exports to average 12.0 billion cubic feet per day (Bcf/d) in 2023. In 2024, with the two new LNG export projects, we expect LNG exports to increase to 13.3 Bcf/d. LNG export capacity can be measured in two ways: nominal, or nameplate, capacity and peak capacity. Nominal capacity is the volume of LNG produced in a calendar year under normal operating conditions, based on the engineering design of a facility. Peak capacity is the volume of LNG produced under optimal operating conditions, including modifications to production processes that increase operational efficiency. LNG export facilities often operate at more than 100% of their nominal capacity but less than 100% of their peak capacity.

U.S. LNG exporters used 98% of their nominal capacity in 2022, mainly because of the outage at the Freeport LNG facility in Texas and the ramp-up period of the new Calcasieu Pass LNG export facility in Louisiana. We expect U.S. LNG exporters to use 105% of nominal capacity in 2023 and 108% in 2024. These utilization levels are equivalent to 88% and 90% of peak capacity in those years.

The start-up timelines for two new U.S. LNG export projects—both the initial online dates and how quickly they can ramp up exports—are a significant source of uncertainty in our forecast. We expect these two export facilities will come online by the end of 2024 based on public announcements or regulatory filings by project developers.

Data values: U.S. natural gas supply, consumption, and inventories and U.S. Liquefaction Capacity Workbook

Golden Pass Trains 1 and 2 are being built at an existing LNG import terminal in Texas that will be converted into an LNG export facility. This project, which is a joint venture between ExxonMobil and QatarGas, consists of three trains, each with 0.68 Bcf/d of nominal capacity, or 0.80 Bcf/d of peak capacity. According to filings with the Federal Energy Regulatory Commission (FERC), developers plan to bring Trains 1 and 2 into service during the second and fourth quarters of 2024, respectively. Developers plan to bring Train 3 online in the first quarter of 2025, which is currently beyond our forecast horizon.

Plaquemines LNG Phase 1 is a Venture Global project located in Louisiana. Phase 1 consists of 9 blocks, each containing 2 liquefaction trains for a total of 18 liquefaction trains with a combined nominal capacity of 1.3 Bcf/d, or peak capacity of 1.6 Bcf/d. According to FERC filings, developers plan to bring Phase 1 online by the end of 2024 and expect to start LNG production in August 2024.

We estimate Golden Pass Trains 1 and 2 and Plaquemines Phase 1 will add a total of 2.7 Bcf/d of nominal LNG export capacity, or 3.2 Bcf/d of peak capacity. By the end of 2024, U.S. LNG nominal liquefaction capacity will increase to 14.1 Bcf/d and peak capacity to 17.0 Bcf/d across the nine U.S. LNG export facilities.