Economy, weather, and CO2

U.S. macroeconomics

To generate the macroeconomic assumptions in the Short-Term Energy Outlook (STEO), we input STEO energy price forecasts into S&P Global’s Short-Term U.S. Macroeconomic Model to produce a conditional macroeconomic forecast. For more details on the macroeconomic model, see our documentation.

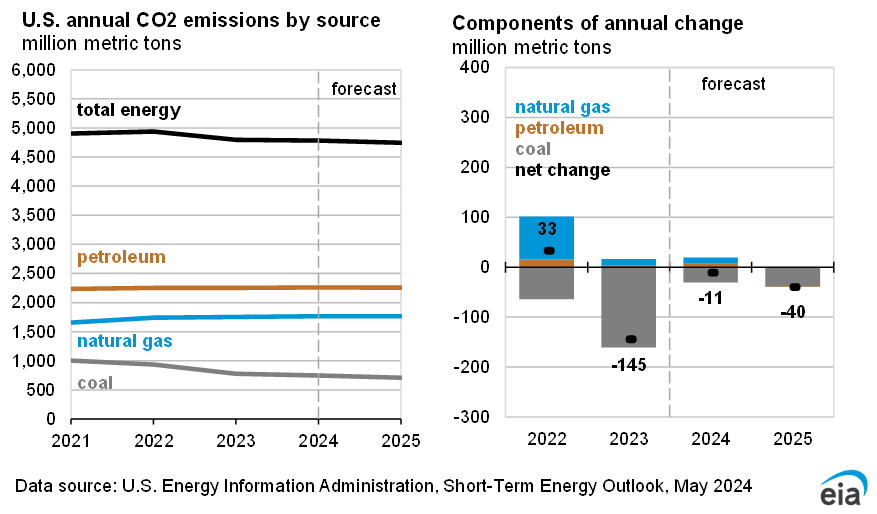

Emissions

We forecast U.S. energy-related carbon dioxide (CO2) emissions to decrease by 1.8% in 2026 relative to 2025 and to increase by a 0.4% in 2027 relative to 2026. In 2026, decreases in CO2 emissions are due primarily to expected declines in coal consumption, most of which occur at power plants for electricity generation. Declines in coal-fired generation and coal-related emissions are expected to continue in 2027 but are counteracted by growth in natural gas-fired generation, resulting in a modest increase in total CO2 emissions.

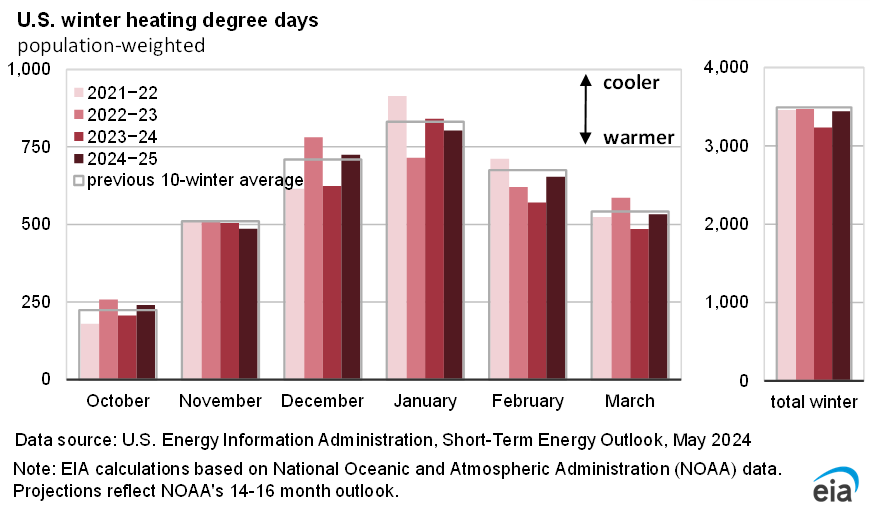

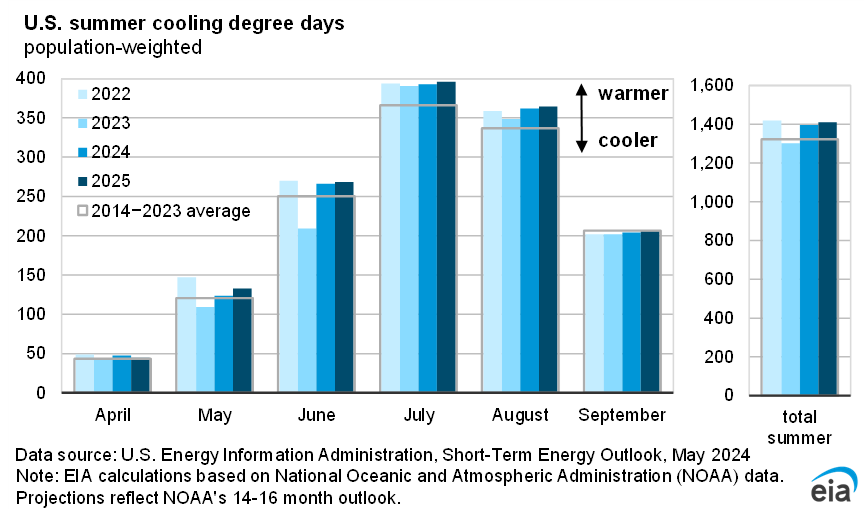

Weather

Our forecast assumes a slightly warmer summer (June–September) in 2025 with 3% more U.S. cooling degree days (CDDs) than the summer of 2025. Based on our current forecasts and data from the National Oceanic and Atmospheric Administration, we expect the United States to average around 240 CDDs in June, 15% fewer CDDs than in June 2025 and 9% fewer than the 10-year monthly average. Warmer weather in the third quarter of 2026 (3Q26) is expected to offset the cooler start to the summer with 8% more CDDs than 3Q25. As a result, we expect the United States will average about 4% more CDDs in 2026 than in 2025 and 4% more than the 10-year average.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}