Global oil markets

Global oil prices and inventories

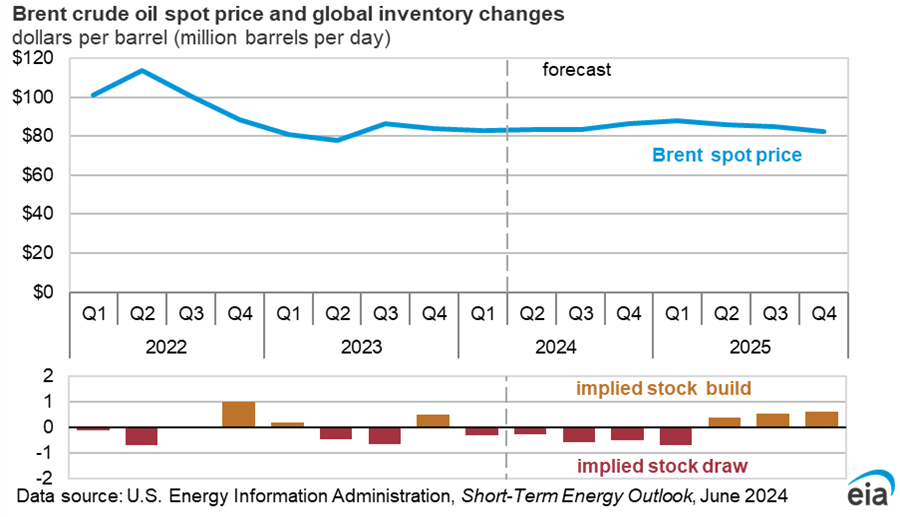

Although short-term prices have sometimes been volatile this year, oil prices have mostly traded within a relatively tight range. The Brent crude oil spot price averaged $82 per barrel (b) in August, marking the eighth consecutive month where it averaged between $80/b and $90/b. Despite a drop in the Brent spot price to $73/b on September 6, we expect ongoing withdrawals from global oil inventories stemming from OPEC+ production cuts will push the price back into that range relatively quickly.

Persistent economic concerns have reduced market expectations around global oil demand growth. Slowing global economic activity and reduced fuel demand in China, one of the leading sources of global oil demand growth, as well as signs of slowing U.S. job growth in recent months, have limited any upward price momentum in recent months.

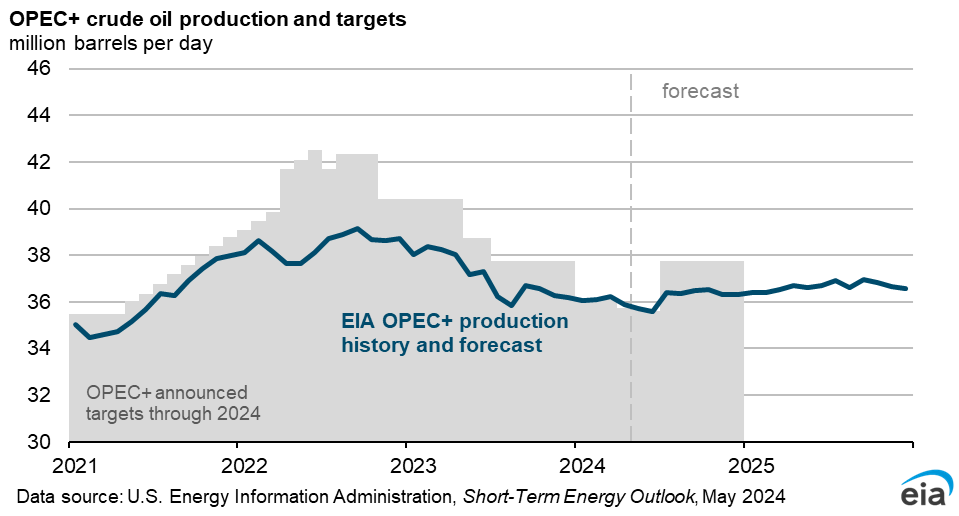

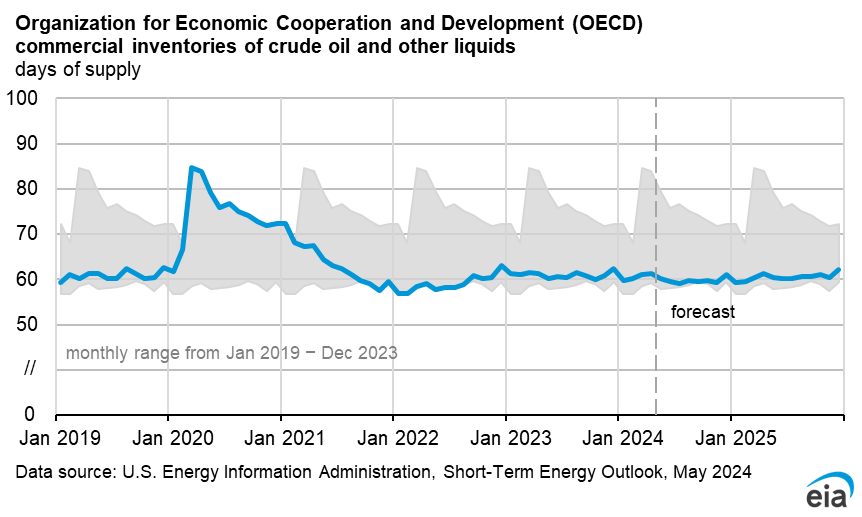

However, we still expect oil prices will rise in the coming months, driven by ongoing withdrawals from global oil inventories as a result of OPEC+ production cuts. The OPEC+ production cuts continue to cause less oil to be produced globally than is being consumed. Even before OPEC+ announced that it will delay production increases until December, we expected a significant reduction in global oil inventories through the end of this year. We now expect more oil will be taken out of inventories than we previously expected.

We estimate global oil inventories are falling by 0.9 million barrels per day (b/d) in 3Q24, and we expect they will decrease by more than 1.0 million b/d through 1Q25. As a result, we expect Brent prices will rise from $74/b at the beginning of September to average $82/b in December and $83/b in 1Q25.

By mid-2025, we anticipate that the market will gradually return to moderate inventory builds as OPEC+ increases production through the year and as forecast production growth from countries outside of OPEC+ begins to outweigh global oil demand growth. We estimate that global oil inventories will increase by an average of 0.5 million b/d in the second half of 2025 (2H25). We forecast the Brent price will average $84/b in 2025.

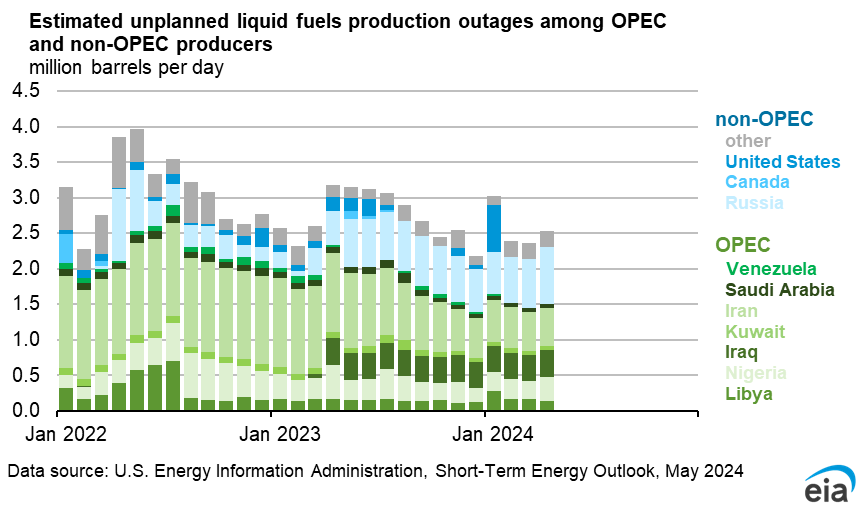

Recent production outages in Libya add a new source of uncertainty for crude oil prices in the coming months. These outages compound existing uncertainties driven by attacks on oil tankers in the Red Sea shipping channel and the possibility the conflict in Gaza spills into neighboring countries, potentially disrupting regional oil production. Similarly, OPEC+ members could further delay the unwinding of voluntary oil production cuts now set to begin in December. Over the long term, whether global oil demand growth will outweigh supply growth from countries outside of OPEC+ remains a key uncertainty.

Global oil production and consumption

The duration of recent disruptions to crude oil production in Libya are a key uncertainty for the oil market in 4Q24. Political unrest and increased tensions between competing Libyan government factions have halted production across numerous oil fields in the country. Estimates are that production fell as low as 0.4 million b/d by the end of August, down from 1.1 million b/d in 1H24. We assume Libya’s oil production will average 0.6 million b/d for the remainder of the year.

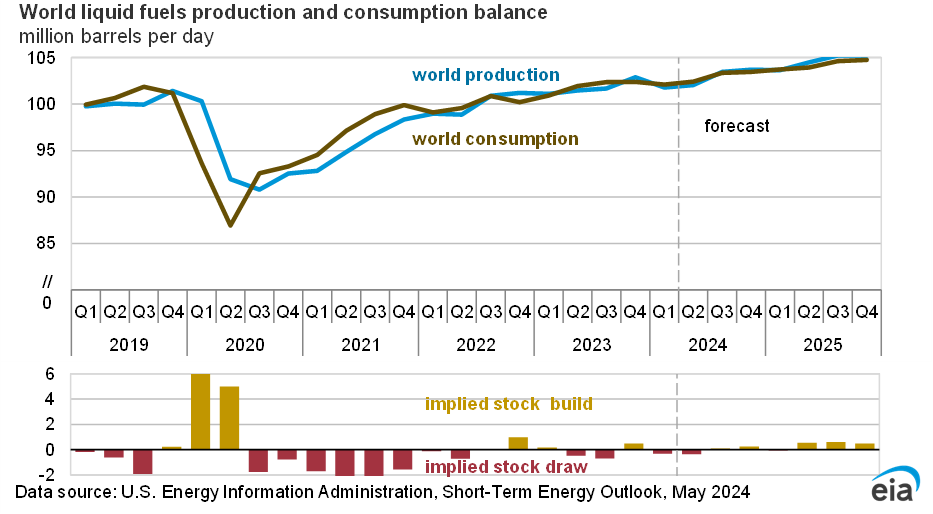

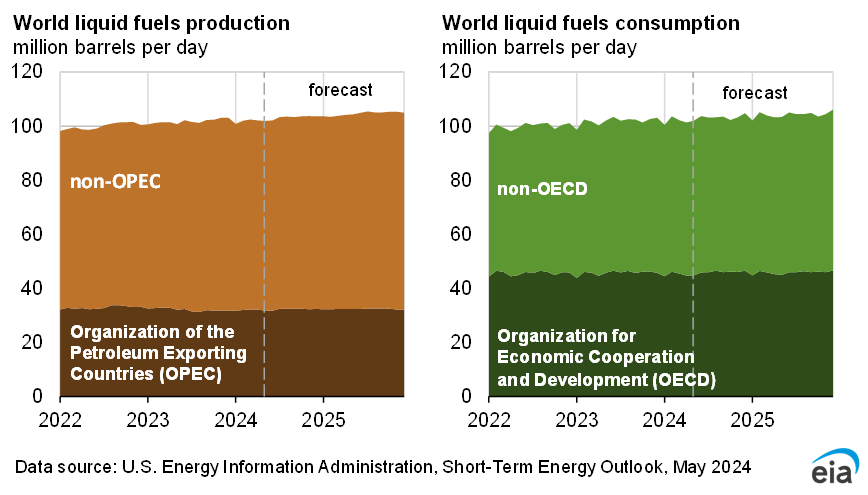

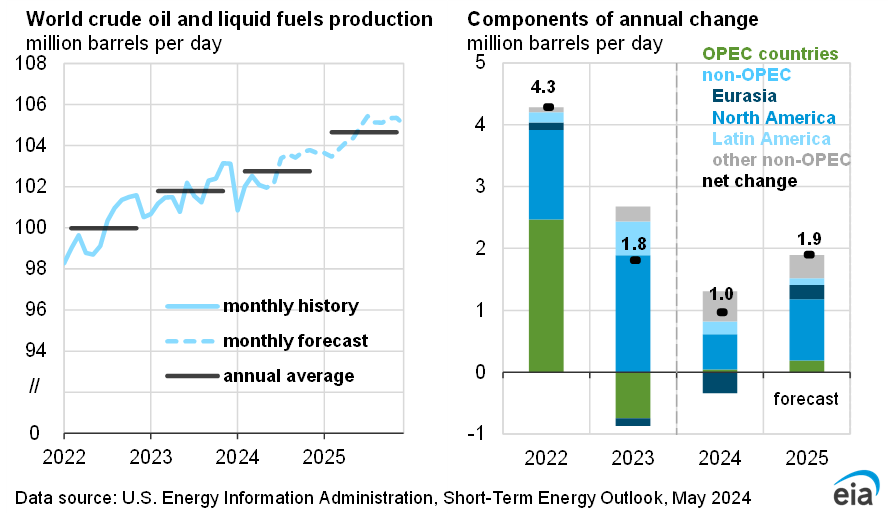

Although OPEC+ cuts and recent productions outages in Libya are limiting world oil production growth, we estimate that growth outside of OPEC+ will remain strong. We expect that global production of petroleum and other liquid fuels will increase by 0.3 million b/d in 2024. OPEC+ liquid fuels production in our forecast decreases by 1.4 million b/d in 2024, while production outside of OPEC+ increases by 1.7 million b/d, led by growth in the United States, Canada, Guyana, and Brazil. Global production of liquid fuels increases by 2.4 million b/d in 2025, with OPEC+ production increasing by 0.8 million b/d and 1.6 million b/d of production growth from countries outside of OPEC+.

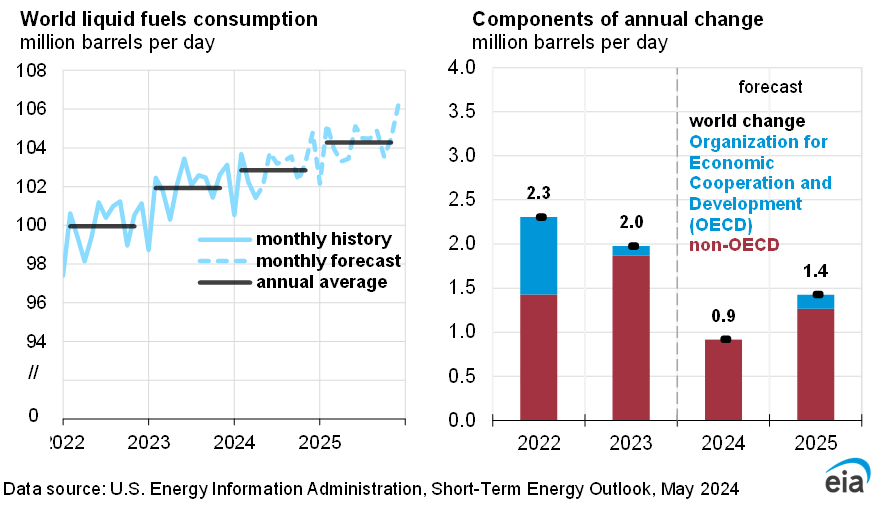

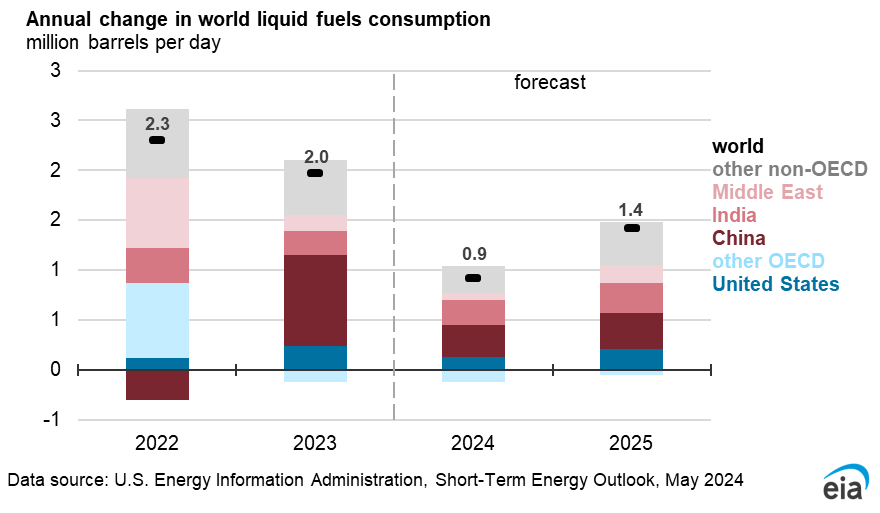

We forecast that global consumption of liquid fuels will increase by 0.9 million b/d in 2024 and 1.5 million b/d in 2025. Our 2024 forecast is down 0.2 million b/d from last month and our 2025 forecast is down 0.1 million b/d due to downward revisions to demand in China and OECD Europe. Most of the expected liquid fuels demand growth is from non-OECD countries, which increase their liquids consumption by 1.0 million b/d in 2024 and 1.3 million b/d in 2025. We revised our forecast petroleum consumption growth in China for 2024 and 2025 down because of slower economic activity as well as new monthly statistics showing a slowdown in diesel demand, jet fuel consumption, and crude oil refinery runs in China. We now forecast China’s petroleum and liquid fuels consumption will grow by about 0.1 million b/d in 2024 and 0.3 million b/d in 2025.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}